Copyright © 2024 Swire Pacific Limited. All rights reserved.

Cookies and Privacy: We use cookies to enhance your user experience on our website. Please indicate your cookie preference. For more information, please read our Cookie Policy and Privacy Notice.

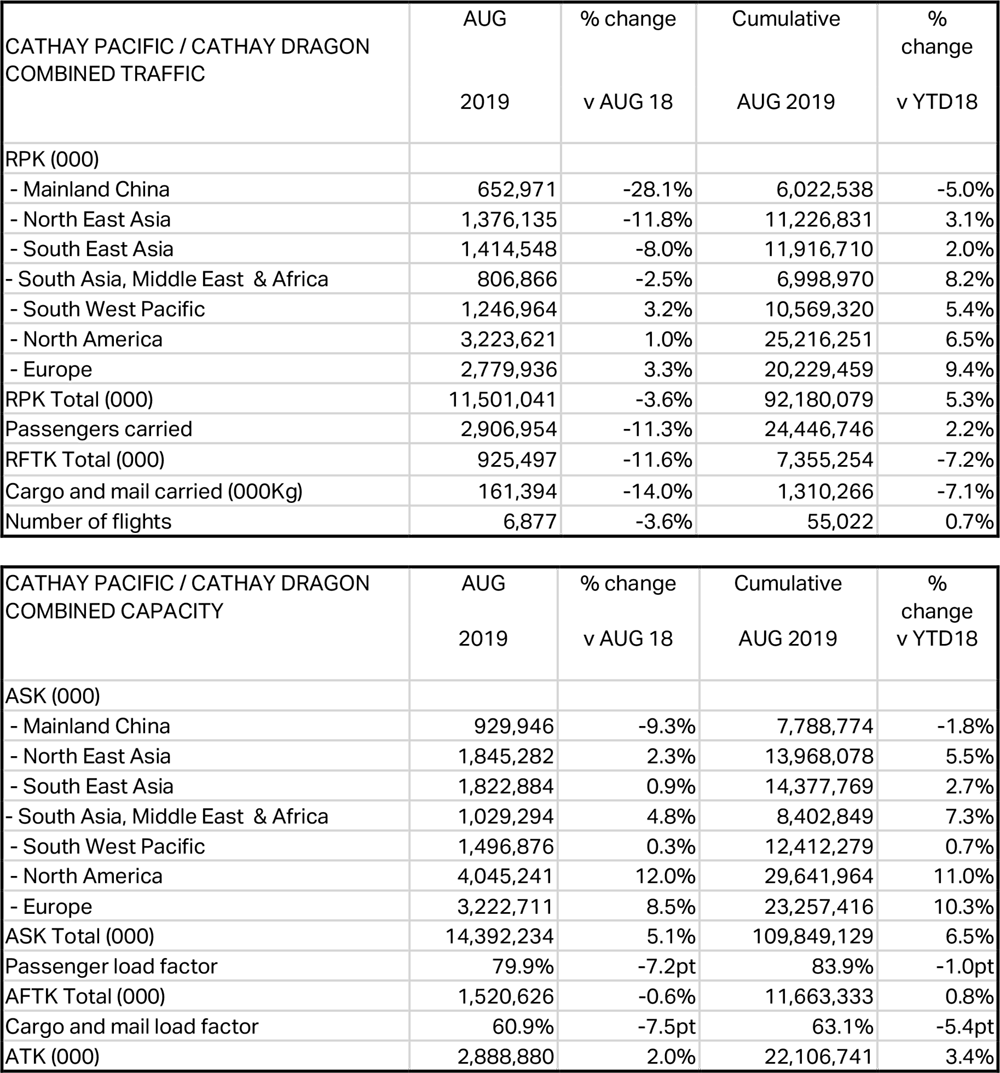

Cathay Pacific Group today released combined Cathay Pacific and Cathay Dragon traffic figures for August 2019 that show decreases in the number of passengers carried and the amount of cargo and mail uplifted compared to the same month in 2018.

Cathay Pacific and Cathay Dragon carried a total of 2,906,954 passengers last month - a drop of 11.3% compared to August 2018. Passenger load factor decreased by 7.2 percentage points to 79.9%, while capacity, measured in available seat kilometres (ASKs), rose by 5.1%. In the first eight months of 2019, the number of passengers carried grew by 2.2% and capacity increased by 6.5%, as compared to the same period for 2018.

The two airlines carried 161,394 tonnes of cargo and mail last month, a drop of 14% compared to the same month last year. The cargo and mail load factor fell by 7.5 percentage points to 60.9%. Capacity, measured in available freight tonne kilometres (AFTKs), was down by 0.6% while cargo and mail revenue freight tonne kilometres (RFTKs) dropped by 11.6%. In the first eight months of 2019, the tonnage fell by 7.1% against a 0.8% increase in capacity and a 7.2% decrease in RFTKs, as compared to the same period for 2018.

Cathay Pacific Group Chief Customer and Commercial Officer Ronald Lam said, "August was an incredibly challenging month, both for Cathay Pacific and for Hong Kong. Overall tourist arrivals into the city were nearly half of what they usually are in what is normally a strong summer holiday month, and this has significantly affected the performance of our airlines. Our inbound Hong Kong traffic was down 38% while outbound was down 12% year-on-year, and we don’t anticipate September being any less difficult.

"Demand for premium class travel experienced a more significant drop relative to leisure travel and overall load factor dipped significantly to 80%. Inbound traffic demand to Hong Kong from regional markets, particularly mainland China and North East Asia, was severely hit, though our South Pacific routes were a bright spot. As a result of reduced travel demand, an increased mix of transit passengers and the negative impact caused by the strengthening US dollar, passenger yield was under further pressure.

"Given the current significant decline in forward bookings for the remainder of the year, we will make some short-term tactical measures such as capacity realignments. Specifically, we are reducing our capacity growth such that it will be slightly down year-on-year for the 2019 winter season (from end October 2019 to end March 2020) versus our original growth plan of more than 6% for the period."

"Having said that, we remain optimistic in the medium term. The strong commitment to our brand and customer experience remains unchanged. Our investments in new aircraft and enhancing the customer experience will continue, giving travellers more reasons to fly with us. Customers can look forward to the imminent launch of new First Class and Business Class cabin products as well as a brand new dining proposition to be rolled out in our Economy cabins. Of course, already in place on all cabins on long-haul flights is a greatly expanded inflight entertainment offering."

"On the cargo side, our business continued to face headwinds. Tonnage further deteriorated month-on-month across all regions, driven in particular by slow demand over the holiday season in different parts of the world, the effects of tropical storms and disruptions at Hong Kong International Airport. Ongoing geopolitical tensions continued to affect overall market sentiment. Nevertheless, our outlook for September is slightly more positive and we expect to see demand progressively improve, driven by project shipments and the restocking of inventory as we enter the traditionally high-demand season."